Should You Use Debt Consolidation to Pay Off High Interest Credit Cards?

Paying interest, especially high-interest charges on credit cards can be painful. When you find yourself owing on several credit cards, and it becomes harder and harder to make the payments, that’s when you begin to look for some kind of relief. But is debt consolidation right for you?

Debt consolidation, a practice of consolidating all your debts into one with one monthly payment, usually at a lower interest rate, can seem like the right choice. However, there are several things to consider before pursuing this solution to your debt problems.

Paying off high-interest loans and credit cards can be very difficult. A large part of the minimum required payment typically goes toward satisfying the interest, leaving a small amount to pay down the principal.

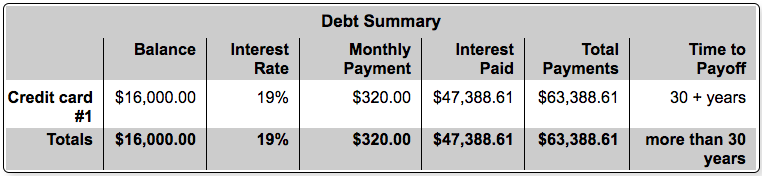

Take a look at the example in the charts below. If you have $16,000 in credit card balances with an average interest rate of 19%, and you pay the standard minimum payment of 2% of the balance, it will take more than 30 years to pay off and cost you $47,388 in interest. The potential profit for creditors is incredibly high. Now you know why they offer 0% and no-interest introductory rates.

Borrowers in these situations naturally look for relief. One of the most common options is debt consolidation because of the potentially lower interest rate and easier-to-manage one-payment option. On the surface, this seems like a no-brainer. Unfortunately, debt consolidation is not always as good as it sounds.

3 factors to consider before using debt consolidation

1. Cost

There’s always a cost to hiring someone to help you solve your problems. No one works for free. Just because you’re able to lower your monthly payment doesn’t mean it’s a good decision. You have to determine what consolidating your debt will actually cost you. Always, always, always, do the math!

Debt consolidation companies charge a fee. If the fee is more than what you’re saving in interest, avoid this option and just pay the debts using a debt snowball plan. Sure, it may be more difficult to manage through multiple payments, but ultimately, paying less and shortening the time should be your primary goal.

2. Time

Lowering the payment alone is not enough. Your goal is to save money while also reducing the time it takes to do so. Don’t sign up for a plan that lowers your monthly payment by lengthening the payoff time over many years. That may actually cost you more money.

You’re looking to make forward progress. Don’t do anything that lengthens the time you’re going to be in debt. The longer your journey to getting out of debt, the more likely you are to quit or regress.

3. Benefit

Debt consolidation can be a benefit only if you address the reason you got into debt in the first place. It doesn't help you change your behavior with money. In fact, it often does the opposite. It lowers your payment freeing up some of the money that was going towards the minimum payments.

You now have extra money and newly available credit made possible by paying off all those credit cards. If you got into debt because you overspent on credit cards, creating more spending power on your credit cards can be a dangerous strategy.

Focusing on the symptom [debt] instead of the real problem [overspending] is the reason most people don’t benefit when they use debt consolidation or file for bankruptcy. Working through paying off your own debt provides the time you need and the appropriate level of pain and discomfort to create lasting change.

Conclusion

If you’re committed to paying off your debt, I just want to say, “Good for you!” It’s going to take effort and a good plan to succeed, and I know you can do it. Whether you’re ready to use a debt consolidation plan or do it on your own is up to you. What’s important is that you start NOW!

Don’t put it off any longer. If you need help, the debt tools on my resource page can help. You’ll also need to have a plan for managing your expenses to avoid debt in the future. If you don’t yet have a written budget, you can find a step-by-step guide in this blog.

I’m cheering you on!